Singapore's 2026 FATF Report Shows Where Hong Kong's Next Compliance Questions Will Land

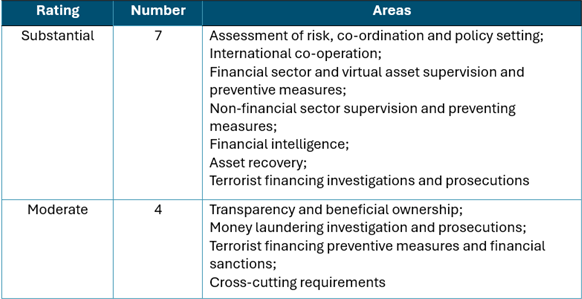

Singapore's May 2026 Financial Action Task Force (FATF) report is the first 5th Round assessment of a major Asian international financial centre, making it a useful regional benchmark. Its seven Substantial and four Moderate ratings reflect a broadly strong AML/CFT framework, while also showing where FATF scrutiny is evolving. For Hong Kong financial institutions, it offers an opportunity to learn from a closely comparable market that shares many of the same characteristics as a global financial centre, trade hub, wealth management market and gateway for cross-border capital.

Singapore's FATF Assessment: Four Moderate Areas Stand Out

FATF uses 11 Immediate Outcomes to assess effectiveness in practice. Singapore received no “Low” ratings, but the four “Moderate” ratings still reveal gaps in execution and verification.

Four Gaps that Matter for Hong Kong

Beneficial ownership verification: self-declared information is not enough

In Singapore, beneficial ownership challenges were linked less to data collection than to data verification and accessibility. Central register information was often not independently verified, foreign companies and Variable Capital Companies (VCCs) showed information gaps, trusts were not covered by a central register, and around 1% of company’s ownership was not traced through beyond a foreign legal entity to the ultimate natural person.

In Hong Kong, the same issue is likely to carry significant weight. What increasingly matters is not only whether ownership information has been collected, but whether it can be verified independently, maintained as circumstances change and evidenced clearly in practice.Money laundering beyond fraud

Singapore opened 11,189 money laundering investigations over five years, but only 682 individuals were prosecuted, implying a conversion rate of below 10 percent. More than 80 percent of the caseload was driven by scam-related complaints, with lower value money mule cases absorbing significant investigative resources. By contrast, higher risk areas such as Trade Based Money Laundering (TBML), tax crime, corruption, professional intermediaries and complex cross-border networks saw much less visible enforcement.For Hong Kong, the question is not how many cases are opened, but whether enforcement outcomes extend to the more complex typologies that matter most in the local market. That includes trade-based laundering, intermediary enabled structures and broader cross border networks.

Sanctions execution and speed

Singapore’s report highlights a gap between sanctions framework and sanctions execution. No assets were frozen under UNSC 1267, and only SGD 1.3 million under UNSC 1373, while FATF found that dissemination chains were too slow and not always completed within 24 hours.Against Hong Kong’s expanding regulatory perimeter, including licensed stablecoin issuers, the practical challenge is becoming clearer. What matters is not only whether sanctions screening is in place, but whether institutions can demonstrate timely and consistent action, supported by a clear audit trail.

Proliferation financing (PF) and digital asset exposure

Singapore received 1,900 PF related suspicious transaction reports, including 732 linked to North Korea, but froze only SGD 22.3 million, most of it in a single case. FATF also identified limited supervisory coverage for Virtual Asset Services Provider (VASP) and Cash-Secured Put (CSP), as well as very low awareness among some foreign flag state representative offices.

In Hong Kong, this issue is becoming more relevant as trade connectivity, maritime activity and regulated digital asset growth increasingly intersect. With the first stablecoin licenses issued in April 2026, PF exposure across cross border flows deserves closer assessment, particularly where corporate structures and digital asset channels overlap.

The Shift from Framework to Proof

Under FATF's 2022 Methodology, the focus has shifted from the existence of rules and controls to whether they can be demonstrated in practice. This places greater emphasis on verifiable data, supporting documentation and clear audit trails. The issue is increasingly not whether a legal or policy framework exists, but whether institutions and authorities can substantiate ownership information, identify higher-risk activity and evidence the consistent execution of key controls in practice.

Data Infrastructure for Evidence Led Compliance

Responding to FATF's increasing focus on verification and demonstrable outcomes requires more than policy design alone. It requires data infrastructure that can support ownership validation, risk visibility, and clearer evidential trails. Dun & Bradstreet contributes to this through global corporate data, the D‑U‑N‑S® Number, Ultimate Beneficial Owner (UBO) intelligence, Corporate Linkage, adverse information, and network analytics that help strengthen Finance Crime Compliance (FCC) frameworks across entities, ownership, jurisdictions, and business activities.

UBO verification

D&B's global corporate ownership data, covering more than 430 million entities, enables institutions to trace from a single legal entity to the ultimate beneficial owner and across related entities within the wider corporate structure. This provides an independent source of corroboration beyond customer-supplied information and supports stronger verification of ownership data.Related asset expansion

Using ownership and control mapping, institutions can identify the control structures of sanctioned individuals and entities, allowing them to move beyond freezing only directly held assets and toward tracing and immobilizing related assets linked through ownership or control relationships. This supports a more complete and timely response to sanctions and related exposure.Trade Based Money Laundering (TBML) cross validation

By combining D&B's global bill of lading data with business activity and trade profile intelligence, institutions can cross-check counterparties against trade background and logistics information. This helps identify commercial risks and narrow the information gap between financial flows and underlying goods flows.Professional intermediary network detection

Relationship mapping across directors, shareholders and authorized signatories can reveal hidden links such as shared directors, nominee shareholders and repeated cross appointments across multiple entities. This supports stronger identification of intermediary networks and more advanced Anti-Money Laundering (AML) risk detection.

Singapore's report should be read as a useful reference point for how FATF expectations are evolving. With Hong Kong's next 5th Round mutual evaluation scheduled for 2029–2030, it offers a valuable opportunity to learn from a sophisticated and closely comparable international financial centre and to prepare more deliberately for the next round of assessment.

>>Download FAFT Mutual Evaluation of Singapore full report here.