2025-2026 Enforcement Wave: Compliance Starts with Knowing Your Customer

Since 2025, regulators have made one expectation clear: customer identification is not a routine onboarding step. It is the foundation of effective compliance.

Across Chinese Mainland and Hong Kong, enforcement has become more frequent, more detailed, increasingly extend to senior management accountability. In Hong Kong, HKMA disciplinary actions against banks and SVF licensees reflect the same approach. The focus is no longer simply on whether controls exist, but on whether customer due diligence and ongoing monitoring are carried out in a way that is genuine, verifiable and traceable.

2025 to 2026 Enforcement Snapshot (Chinese Mainland and Hong Kong) Chinese Mainland: From Customer Identification Failure to End-to-End KYC Breakdowns

2025 marked a shift from isolated penalties to lifecycle scrutiny, from onboarding through transaction monitoring. Regulators are no longer citing single control gaps. They are linking weaknesses across the customer journey, including customer identification, record retention, and traceability.

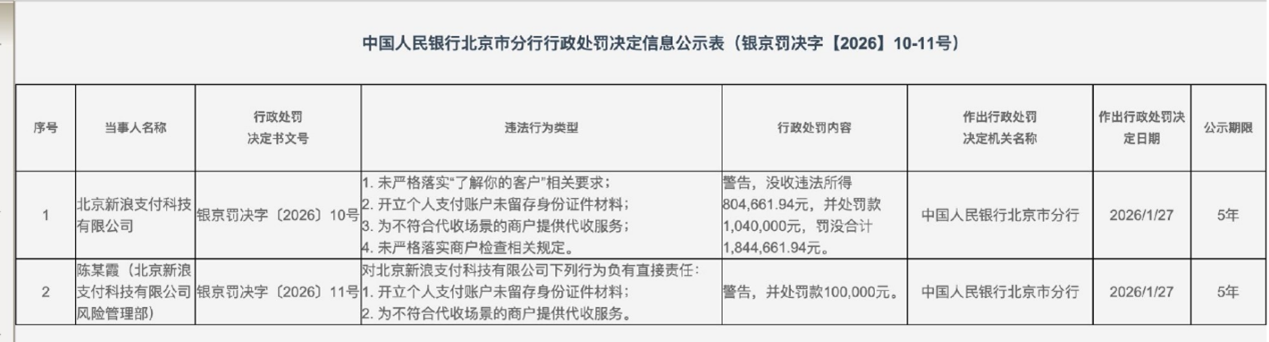

Shengdi jia Payment, Huiju Payment, and Sina Payment were penalized in 2025-2026 for failure in customer identification, record retention, and traceability transaction with dual penalties

Source: Sina Finance (2026, January 31)

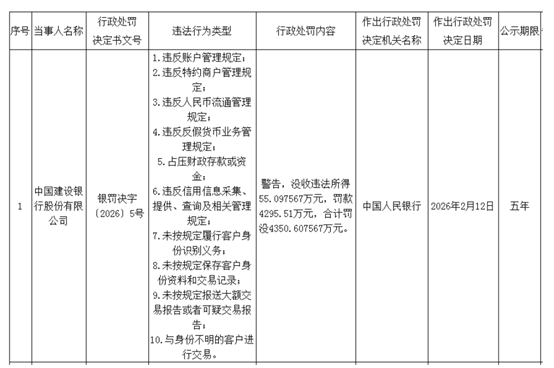

China Construction Bank and Shanghai Pudong Development Bank were penalized by the People's Bank of China on 14 February 2026, with actions extending to multiple managers. Key issues included customer identification failures, record retention gaps, and transactions with unidentified customers. Both banks received penalties exceeding RMB 40 million.

Source: nb.ifeng.com (2026, February 24)

A consistent theme is that regulators increasingly treat AML breaches and operational governance failures as one systemic breakdown in a single KYC control chain.

Hong Kong: Fewer Cases, Clearer Signals

Compared with Chinese Mainland, Hong Kong has seen fewer disciplinary actions, but each case sends a clear signal. In July 2025, the HKMA reprimanded and fined 33 Financial Services Limited, an SVF licensee, HK$1.6 million, citing gaps in understanding the purpose of business relationships, inadequate CDD on represented entities, and weak controls and record keeping where verification was performed by outsourced or partner parties.

Source: HKMA (2025, July 22)

In Hong Kong, the question is not only who the customer is, but whether the institution truly understands the corporate entity behind the relationship.

Root Causes of Enforcement (Breakdowns Across the KYC and KYB Chain)

Across both Chiense Mainland and Hong Kong, enforcement actions point to three basic failures.

Who the customer is: gaps in enterprise identity verification

Regulators frequently cite:

- Failure to perform customer identification

- Transactions conducted with unidentified customers

- Failure to conduct CDD on the represented entity

The core gap is an inability to independently prove that the enterprise exists and remains active. Customer submitted documents alone are no longer sufficient.Who represents and controls the business: Decision cannot be reconstructed

Common issues include:

- Insufficient verification of the intention to open corporate accounts

- Weak merchant real-name authentication

- Missing or non‑reproducible approval logic for authorized

What regulators want is not just proof that documents were collected, but whether the institution can later reconstruct its decision and the evidence behind it.Ongoing due diligence is weak: Monitoring cannot support risk detection

Many cases expose a structural disconnect:

- Customer information is not kept up to date

- Suspicious transactions are not identified and reported in a timely manner

- Transaction information is not sufficiently accurate, complete, or traceable

What this exposes is not simply a systems weakness, but a structural disconnect between front end KYB and back-end monitoring.

Embedding KYB into Workflow: Verify, Map, Monitor

In Hong Kong, understanding a corporate customer must go beyond onboarding. It needs to be evidenced, maintained, and capable of regulatory review. Under the HKMA approach, effective CDD and KYB come back to three questions.

Who is the customer?

What is the entity behind the customer?

Can the institution demonstrate ongoing control?

That is why Hong Kong enforcement pays close attention to the purpose and nature of the relationship, the entity represented by the customer, and whether the institution can produce evidence to support that understanding. KYB is not a formality. It is how control is demonstrated. Therefore, making KYB verifiable and scalable is not about collecting more documents, but embedding KYB into operation workflow. Dun and Bradstreet supports this across three areas:

Enterprise Identity Verification

- Independently verify legal existence, registration status, and consistency of enterprise information

- Reduce reliance on customer self‑declaration

- Establish a durable identity baseline for onboarding decisionsCorporate Relationship and Control Visibility

- Map parent–subsidiary structures and group relationships

- Support UBO and control‑chain analysis

- Enable coherent narratives linking individuals, enterprises, and authorityContinuous Monitoring and Trigger‑Based Review

- Monitor enterprise lifecycle changes, risk events, and AML screening outcomes

- Automatically trigger reassessment when risk‑relevant changes occur

- Generate audit‑ready evidence to support due diligence

Global Registry Data: KYB That Regulators Can Verify

Effective KYB depends on reliable, independently sourced enterprise data. Dun & Bradstreet's Global Registry Data integrates official company registration information and original documents across over 100 countries and regions via API. It supports essential enterprise identity attributes, including legal status, directors, and ownership structures, enabling organizations to:

Perform KYB using independent, authoritative sources

Preserve evidence trails that can withstand regulatory review

Scale enterprise verification without proportional increases in manual workload

In today's regulatory environment, this capability is no longer optional.

KYB as Financial Infrastructure

Regulators are no longer judging compliance by the presence of procedures, but by the strength of the evidence behind them. That shift is making KYB a core capability for safe growth, built on enterprise identity and corporate relationship data that stands up to review and works in day-to-day operations. Fines are not the end point. They are the signal that the standard has changed.